Stablecoin settlement, tokenized deposits, real-world assets, and private DLT rails all create the same institutional requirement: banks need a compliance layer that can connect identity, wallet activity, approvals, signing, monitoring, and audit evidence. Without that layer, digital asset products remain difficult to scale beyond pilots.

A digital asset compliance toolkit is the control architecture that helps banks manage AML, KYC, wallet screening, transaction monitoring, governance, case workflows, and regulator-ready reporting across blockchain-based activity. It is not a single vendor dashboard. It is the orchestration layer that connects existing compliance processes to new digital asset infrastructure.

This matters because blockchain changes the shape of compliance work. Transactions can be fast, irreversible, and pseudonymous. Wallets do not carry inherent customer identity. Raw hashes do not explain business context. Compliance teams need systems that translate on-chain activity into bank-grade risk decisions and audit records.

Why Digital Asset Compliance Becomes the Gating Layer

Banks can only scale digital asset products once custody, compliance, and controls are standardized. The technical ability to move assets on-chain is not enough. Risk teams need to know who owns a wallet, who approved a transaction, whether a counterparty is allowed, how AML screening was performed, and what evidence supports the decision.

The regulatory direction supports this view. FATF's virtual asset guidance applies the Travel Rule to virtual asset service providers, requiring originator and beneficiary information to be obtained, held, and transmitted for virtual asset transfers. See FATF's virtual assets guidance. In the EU, the European Banking Authority has published guidelines under Regulation (EU) 2023/1113 covering information requirements for transfers of funds and certain crypto-asset transfers. See the EBA's transfer information requirements guidelines.

This applies across multiple digital asset use cases:

- Stablecoin settlement and treasury flows.

- Tokenized deposit issuance and redemption.

- Tokenized money market funds, treasuries, bonds, and private credit.

- RWA lifecycle management.

- Internal settlement on private DLT rails.

- Interbank or consortium settlement networks.

Each use case introduces new data paths. Identity may live in onboarding systems. Wallet control may live in custody infrastructure. AML risk may come from blockchain analytics. Approvals may sit in policy engines. Transaction hashes may live on-chain. Case workflows may sit in a GRC or compliance tool.

If those systems remain disconnected, the bank cannot reconstruct the full control story. A production compliance layer must bring them together.

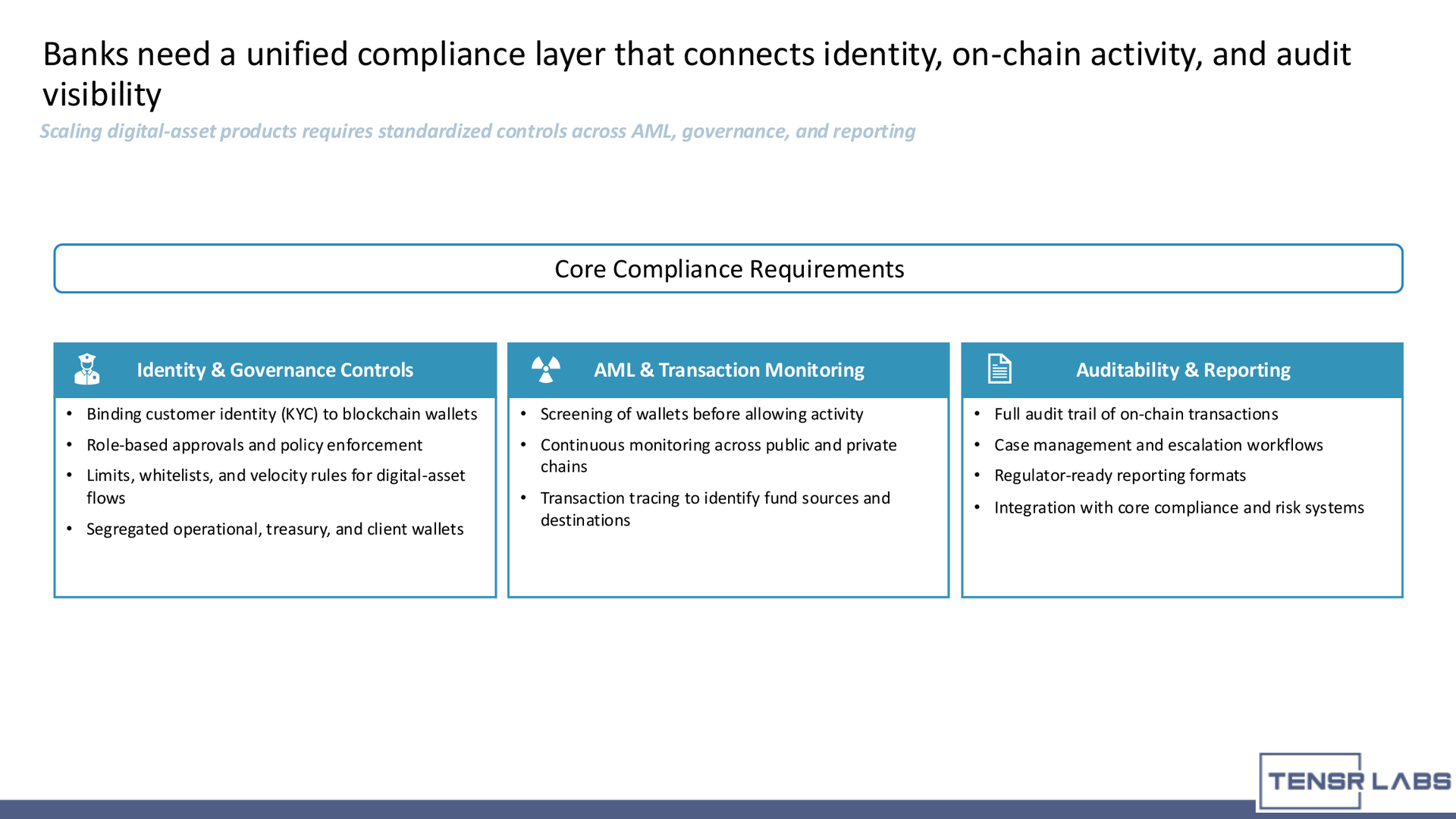

What a Digital Asset Compliance Toolkit Includes

A digital asset compliance toolkit combines controls across identity, transaction monitoring, governance, and reporting. The exact architecture depends on the institution, but the core requirements are consistent.

Identity and Governance Controls

The bank must bind customer identity to blockchain activity. That means connecting KYC, KYB, investor classification, user roles, legal entities, wallet ownership, and transaction privileges.

The compliance toolkit should answer:

- Which customer, entity, or internal desk owns this wallet?

- Which users can initiate or approve activity?

- Which roles apply to this asset, counterparty, amount, and destination?

- Which limits, whitelists, blocklists, or velocity rules apply?

- Are client, treasury, operations, and settlement wallets properly segregated?

Without this identity layer, a wallet is only an address. For a bank, that is not enough.

AML and Transaction Monitoring

Blockchain AML requires screening and monitoring before and after activity. Banks need to assess counterparty wallets, transaction paths, sanctions exposure, illicit clusters, mixers, bridges, high-risk services, and unusual behavior.

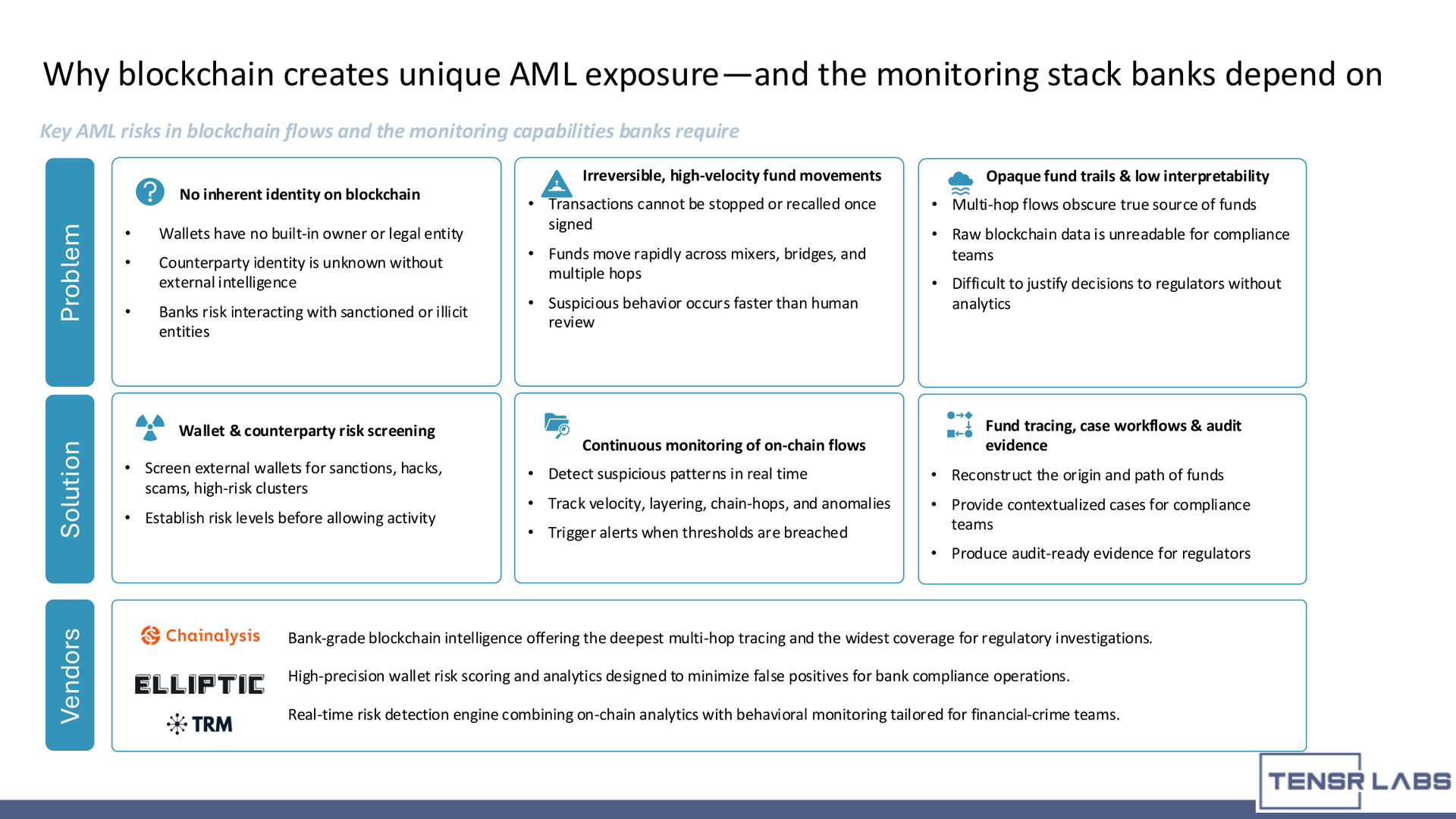

This is not theoretical tooling anymore. Chainalysis KYT is positioned around transaction monitoring, alerts, risk settings, and case management. TRM Labs describes transaction monitoring, wallet screening, and blockchain intelligence across on-chain transfers. Elliptic provides wallet screening and transaction monitoring across crypto networks. These tools show the shape of the required control stack, even though each bank still has to integrate them into its own policies and systems. See Chainalysis KYT, TRM Transaction Monitoring, and Elliptic transaction monitoring.

Monitoring should support:

- Wallet screening before onboarding or transfer approval.

- Transaction tracing across multiple hops.

- Risk scoring for counterparties and source of funds.

- Continuous monitoring across public and private chains where relevant.

- Case creation and escalation workflows.

- Alerts based on amount, velocity, geography, asset type, counterparty, or behavioral anomalies.

Traditional AML systems often were not built to interpret blockchain data directly. The compliance toolkit must enrich those systems with digital asset context.

Auditability and Reporting

Auditability is where many digital asset pilots fail. It is easy to show a transaction hash. It is harder to show the full institutional record: who initiated the transfer, who approved it, which policy applied, which checks passed, which custody signer executed it, which chain event finalized it, and how the result reconciled to internal systems.

A bank-grade toolkit should produce a single evidence trail that connects:

- Customer or entity identity.

- Wallet ownership.

- Initiation request.

- Policy checks.

- Approvals and overrides.

- Custody signing events.

- On-chain transaction data.

- AML monitoring outputs.

- Case notes and escalation decisions.

- Final settlement and reconciliation.

This is what regulators and internal audit teams need: not isolated logs, but a coherent record of control.

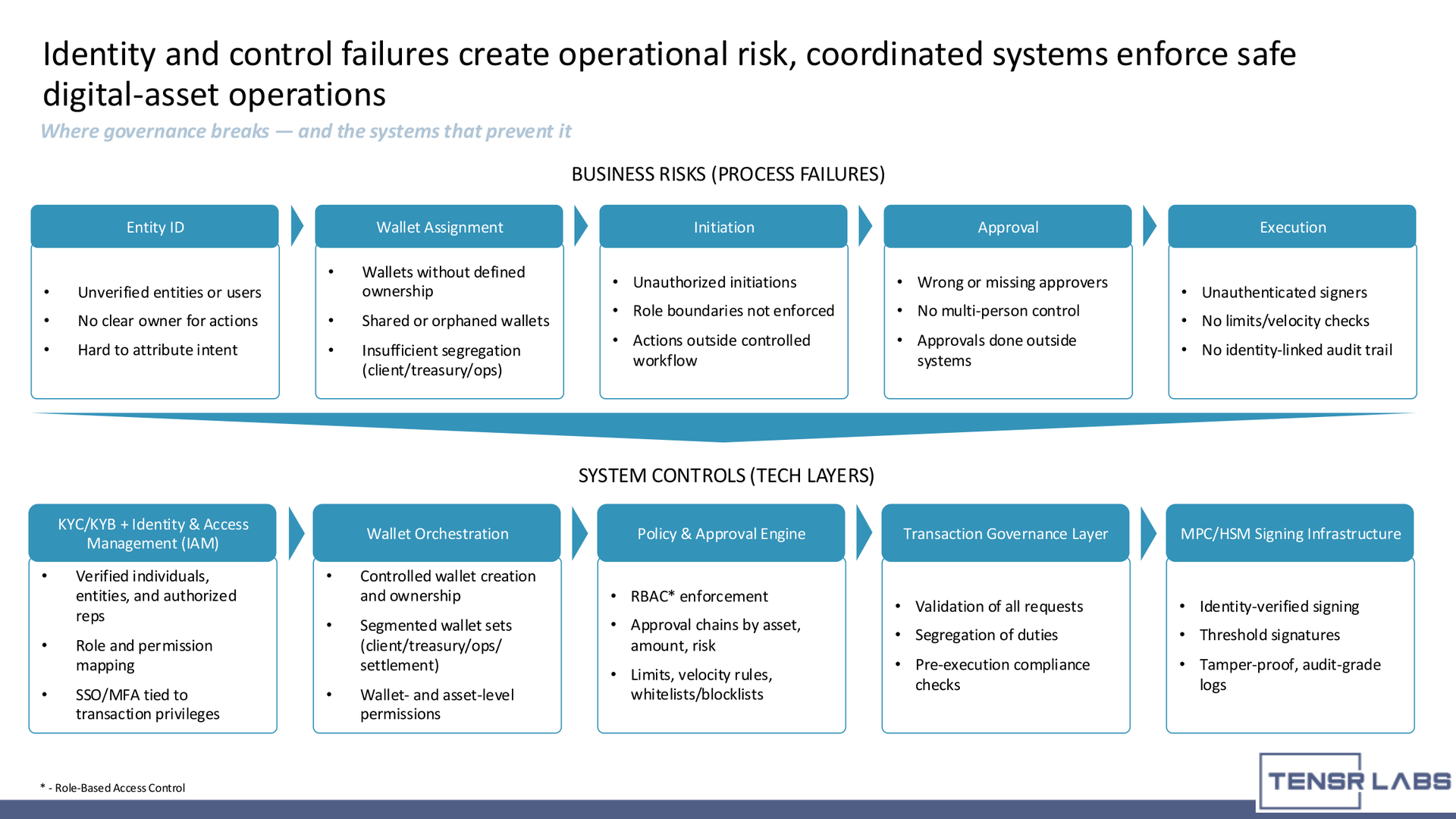

Connecting KYC/KYB, IAM, and Wallet Ownership

The first digital asset compliance challenge is identity. Blockchain wallets do not inherently reveal the legal person, institution, authorized representative, or internal business unit behind them. Banks must create that mapping.

A strong model connects KYC/KYB and IAM to wallet orchestration:

- The customer, counterparty, investor, or internal entity is verified.

- Authorized users and representatives are linked to roles.

- Approved wallets are assigned to the entity or product.

- Wallet permissions are scoped by asset, jurisdiction, product, and use case.

- SSO, MFA, and IAM privileges are tied to transaction rights.

- Every initiation, approval, and execution is logged against identity.

This prevents common control failures: orphaned wallets, shared credentials, unauthenticated signers, approvals outside systems, missing owners, and unclear accountability.

For banks, wallet ownership is not a technical detail. It is the bridge between compliance policy and blockchain execution.

AML and Transaction Monitoring for Blockchain Flows

Blockchain creates unique AML exposure because value can move quickly across wallets, bridges, exchanges, mixers, smart contracts, and multiple networks. Compliance teams cannot rely only on raw transaction hashes or manual review.

The most common risks include:

- Unknown wallet ownership.

- Counterparty exposure to sanctioned or illicit entities.

- Multi-hop fund trails that obscure source of funds.

- Rapid layering across chains or services.

- Irreversible transactions after signing.

- Lack of business context in raw on-chain data.

The monitoring stack should convert these risks into usable compliance workflows. Platforms such as Chainalysis, Elliptic, TRM Labs, and other blockchain intelligence providers can support wallet screening, risk scoring, fund tracing, and alert generation. The important point is that these tools need to connect to bank workflows, not operate as disconnected dashboards.

A practical monitoring workflow looks like this:

- Screen external wallets before allowing activity.

- Establish a risk level and policy decision.

- Monitor transactions continuously after onboarding.

- Detect suspicious patterns such as layering, velocity spikes, high-risk clusters, or bridge activity.

- Create contextual cases for compliance review.

- Store the evidence and decision trail for audit.

This turns blockchain analytics into a bank compliance process.

Governance Controls: Limits, Approvals, RBAC, and Segregation

AML monitoring is only one part of the toolkit. Digital asset compliance also depends on governance controls that prevent unauthorized or poorly controlled activity before it happens.

Banks need a transaction governance layer that can enforce:

- RBAC and segregation of duties.

- Multi-person approval workflows.

- Limits by asset, wallet, amount, user, entity, and counterparty.

- Velocity rules for high-frequency flows.

- Whitelists and blocklists.

- Pre-execution compliance checks.

- Approved wallet creation and assignment.

- Segmented wallet sets for client, treasury, operations, and settlement.

These controls sit close to custody. If a user initiates a transfer from a treasury wallet to an external address, the custody and policy layer should validate identity, permissions, amount, destination, risk score, approval status, and wallet purpose before signing.

This is the difference between after-the-fact monitoring and real control. Banks need both, but prevention is always stronger than post-event explanation.

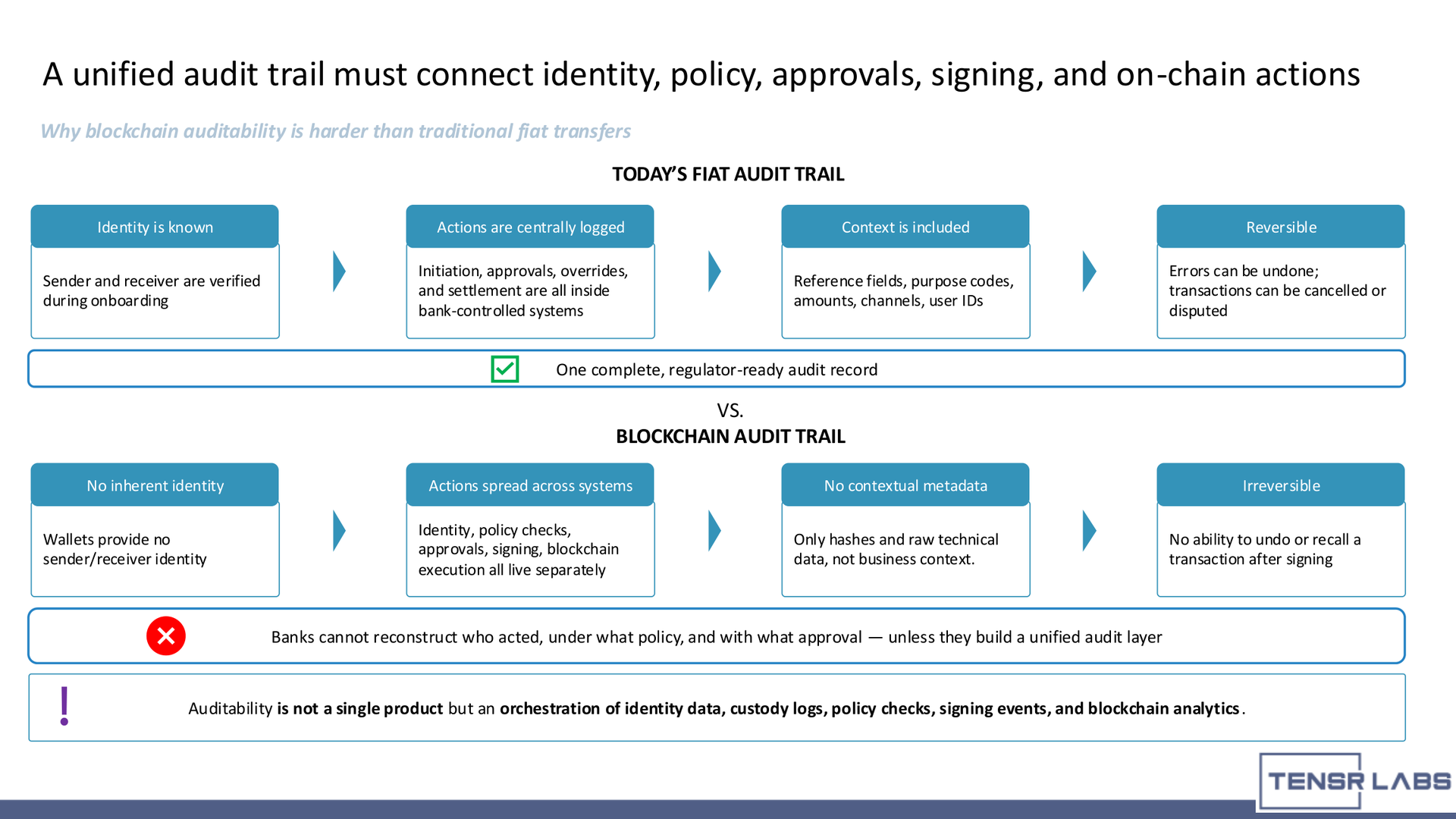

Audit and Reporting: Fiat Rails vs Blockchain Evidence

Traditional fiat transfers usually carry more business context inside bank-controlled systems. Sender and receiver identity are known during onboarding. Reference fields, purpose codes, user IDs, channels, approvals, and settlement events may all sit within internal systems. Errors can sometimes be reversed, cancelled, or disputed.

Blockchain auditability is different. The chain provides a transparent technical record, but that record does not automatically include customer identity, business purpose, approval logic, or compliance context. Transactions may be irreversible after signing. Actions can be spread across identity systems, custody platforms, policy engines, blockchain networks, and case management tools.

This creates a paradox: blockchains are transparent, but bank audit trails can still be incomplete.

A regulator-ready digital asset audit layer must combine on-chain and off-chain records:

- The transaction hash proves execution.

- The custody log proves signing.

- The approval record proves authorization.

- The policy engine proves rules applied.

- The KYC/KYB record proves identity.

- The AML case proves risk review.

- The reconciliation record proves accounting alignment.

Auditability is not a single product. It is the orchestration of identity data, custody logs, policy checks, signing events, blockchain analytics, and bank records.

Vendor Landscape: Analytics Platforms vs Custom Bank Controls

Compliance vendors provide important infrastructure for wallet screening, transaction monitoring, risk scoring, sanctions exposure, tracing, alerts, and case evidence. These tools are essential for many bank digital asset programs.

FATF and EU transfer-of-funds requirements make one point especially clear: compliance teams cannot treat blockchain analytics as optional enrichment. Originator/beneficiary information, wallet risk, transaction context, screening evidence, and case decisions need to travel with the operating workflow. The compliance vendor can provide intelligence, but the bank must still own the policy logic, escalation model, record keeping, and accountability.

But vendors do not define the bank's full operating model. Most customization depends on the bank's business logic, regulatory requirements, product scope, custody stack, approval policies, and existing AML/GRC systems.

When evaluating vendors, banks should ask:

- Which chains, assets, and wallet types are supported?

- How accurate and explainable are wallet risk scores?

- Can alerts be tuned to the bank's risk appetite?

- How are cases exported into existing compliance tools?

- Can the platform support both public-chain analytics and private-DLT workflows?

- How does it integrate with custody approval and signing events?

- Can evidence packs explain decisions to auditors and regulators?

The best architecture treats vendor tools as part of a broader compliance control layer. Screening, monitoring, identity, custody, approvals, and reporting must work together.

How OQTACORE Can Help Integrate Digital Asset Compliance

OQTACORE can help banks and institutional teams design the compliance layer required for production digital asset operations.

At the first stage, OQTACORE can integrate blockchain intelligence tools into wallet screening, transaction monitoring, and case workflows. This helps compliance teams add on-chain visibility without rebuilding their entire AML stack.

At the second stage, OQTACORE can connect identity, policy enforcement, custody approvals, wallet orchestration, AML monitoring, and reporting into one digital asset compliance toolkit. This gives banks a clearer path from KYC/KYB to on-chain execution and audit evidence.

At the enterprise stage, OQTACORE can help design unified audit data orchestration across custody platforms, MPC/HSM signing systems, tokenization engines, private DLT rails, and existing AML/GRC infrastructure.

If your team is preparing to launch stablecoin settlement, tokenized deposits, RWA products, or private DLT operations, the compliance architecture should be designed before production rollout. The goal is not only to detect risk, but to build controls that make safe digital asset operations repeatable.

CTA: Plan a digital asset compliance architecture review with OQTACORE.

References

- FATF, Guidance for a Risk-Based Approach to Virtual Assets and Virtual Asset Service Providers

- European Banking Authority, Guidelines on information requirements for transfers of funds and certain crypto-assets transfers

- ESMA, MiCA interactive single rulebook

- Chainalysis, KYT crypto transaction monitoring

- TRM Labs, Transaction Monitoring

- Elliptic, Crypto transaction monitoring

FAQs

A digital asset compliance toolkit is the control architecture that connects KYC/KYB, wallet ownership, AML screening, transaction monitoring, custody approvals, policy enforcement, case workflows, and audit reporting for blockchain-based financial activity.

Banks need verified wallet ownership, role-based access control, approval workflows, limits, whitelists, wallet screening, transaction monitoring, Travel Rule handling where applicable, case management, custody logs, and regulator-ready audit trails.

Blockchain AML monitoring analyzes wallet risk, transaction paths, source and destination of funds, sanctions exposure, illicit clusters, mixers, bridges, velocity, and suspicious patterns. The output should feed into bank case workflows and audit evidence.

Banks connect KYC/KYB to wallets by verifying customers or entities, assigning approved wallets, mapping authorized users and roles, tying IAM privileges to transaction permissions, and logging every initiation, approval, and execution against identity.

Platforms such as Chainalysis, Elliptic, and TRM Labs can support wallet screening, risk scoring, fund tracing, and transaction monitoring. They should be integrated into the bank’s broader compliance architecture rather than treated as standalone dashboards.