Banks are evaluating digital settlement rails because money movement is changing from delayed messaging and batch reconciliation into programmable, on-chain value transfer. Stablecoins, tokenized deposits, and private DLT settlement networks are no longer only innovation-lab concepts. They are becoming practical options for treasury, payments, liquidity, and capital markets workflows.

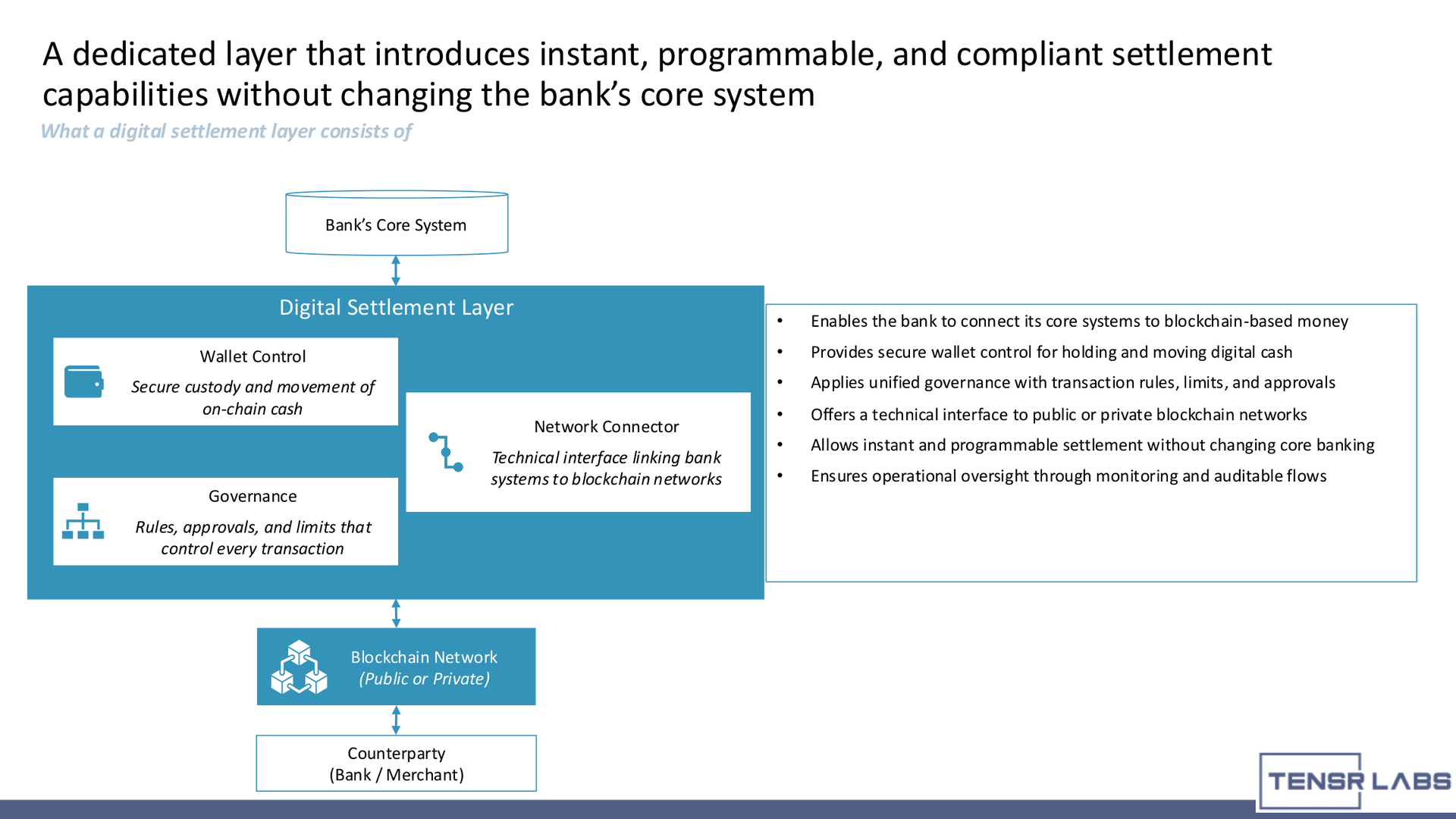

A digital settlement layer is the architecture that lets a bank connect existing core systems to blockchain-based money without replacing the core ledger. It adds wallet control, governance, transaction policies, network connectivity, monitoring, and reconciliation around public stablecoins, bank-issued tokenized deposits, or private DLT settlement networks.

The point is not to abandon banking infrastructure. The point is to create a controlled layer where digital cash can move faster, settle with clearer finality, and remain tied to bank-grade compliance and operational oversight.

What Is a Digital Settlement Layer?

A digital settlement layer is a controlled infrastructure layer that connects a bank's core systems to public or private blockchain settlement rails. It enables instant or near-instant movement of digital cash while preserving governance, wallet security, compliance checks, approvals, monitoring, and reconciliation.

In a bank environment, the layer usually includes:

- Wallet control: secure custody and movement of on-chain cash.

- Governance: transaction rules, approvals, limits, and role separation.

- Network connector: technical interface to public chains, private DLT networks, stablecoin issuers, or interbank networks.

- Compliance controls: wallet screening, AML monitoring, Travel Rule handling where required, and audit evidence.

- Core-system integration: reconciliation with ledger, treasury, payments, and finance systems.

- Operational monitoring: transaction status, exceptions, liquidity visibility, and reporting.

This makes the settlement layer more than a blockchain integration. It is the control plane that lets a bank operate across old and new money rails without losing accountability.

Why Legacy Settlement Rails Create Delay and Operational Risk

Traditional bank settlement is built around messages, correspondent chains, batch cycles, reconciliation, and delayed finality. That architecture works at global scale, but it creates friction for institutions that need faster liquidity, better visibility, and programmable control.

The source presentation highlights familiar operating pain:

- T+1 and T+2 settlement delays.

- End-of-day batch cycles.

- Manual ledger adjustments.

- Reconciliation breaks.

- Value and message mismatches.

- Limited end-to-end traceability in cross-border flows.

- Compliance overhead caused by fragmented visibility across banks.

External data supports the same direction of travel. BIS analysis of SWIFT gpi data found that delays in cross-border payments are often driven not by the payment message itself, but by processing at beneficiary and intermediary banks, including compliance checks, operating hours, and local-market constraints. See the BIS CPMI report on SWIFT gpi data and drivers of fast cross-border payments.

Exception handling is also a real operational burden. SWIFT Payments Market Practice Group guidance on exceptions and investigations exists because payment operations routinely require structured processes for missing details, mismatches, and investigations. See SWIFT's exceptions and investigations market practice guidelines.

Digital settlement layers address this by moving the value leg and the control record closer together. Instead of separating payment instructions, ledger updates, custody movement, and audit evidence across disconnected systems, the bank can orchestrate them through one governed layer.

Three Models for Bank-Grade On-Chain Settlement

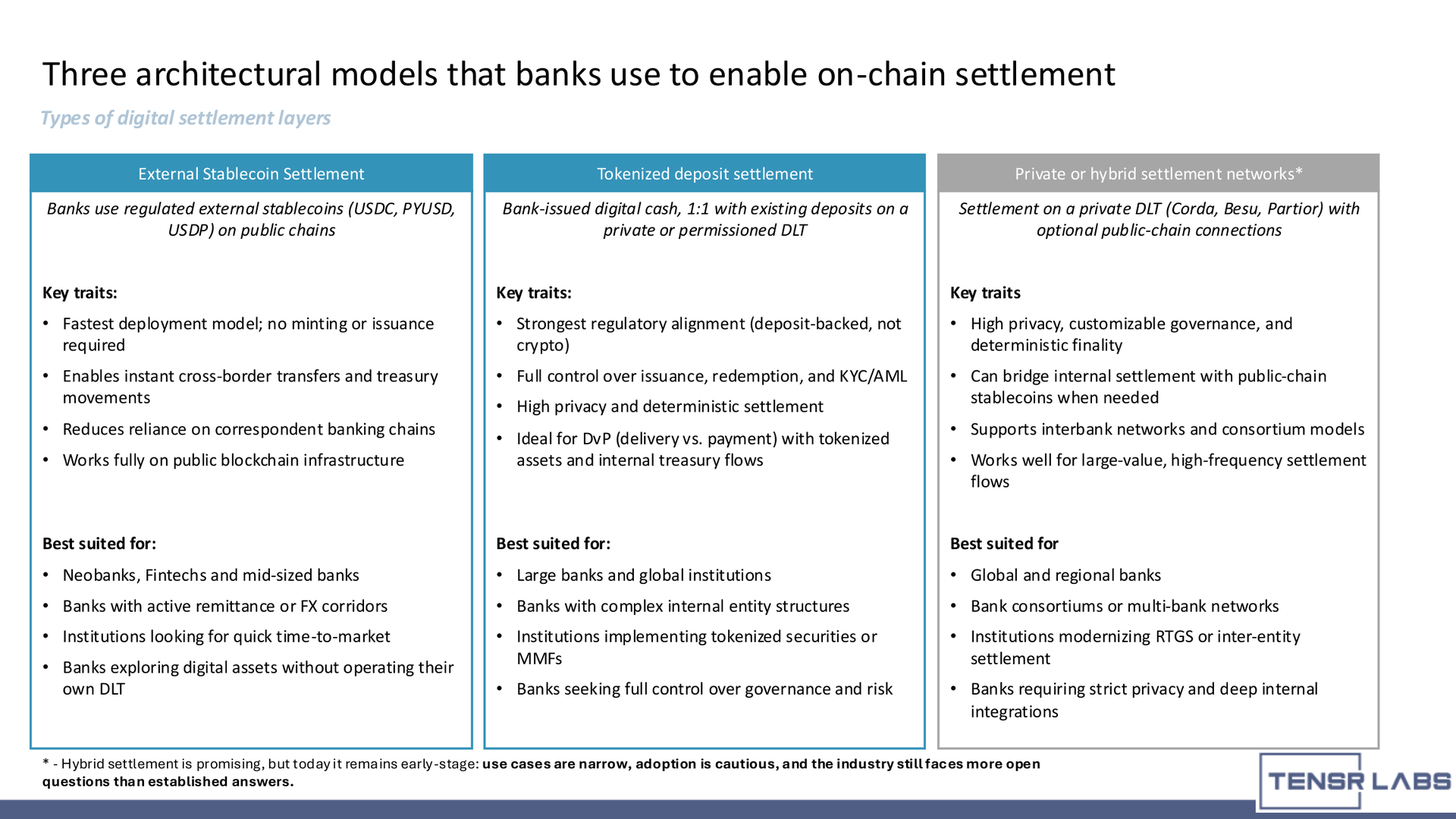

Banks generally evaluate three digital settlement models:

- External stablecoin settlement on public blockchains.

- Bank-issued tokenized deposits on private or permissioned DLT.

- Private or hybrid settlement networks that combine permissioned rails with optional public-chain connectivity.

These models are not mutually exclusive. A regional bank or fintech may start with regulated stablecoins for faster deployment. A large bank may prioritize tokenized deposits for balance-sheet control and DvP use cases. A consortium may need a private network for interbank settlement and shared governance.

The right model depends on the institution's regulatory posture, customer base, use case, privacy needs, liquidity model, custody maturity, and integration capability.

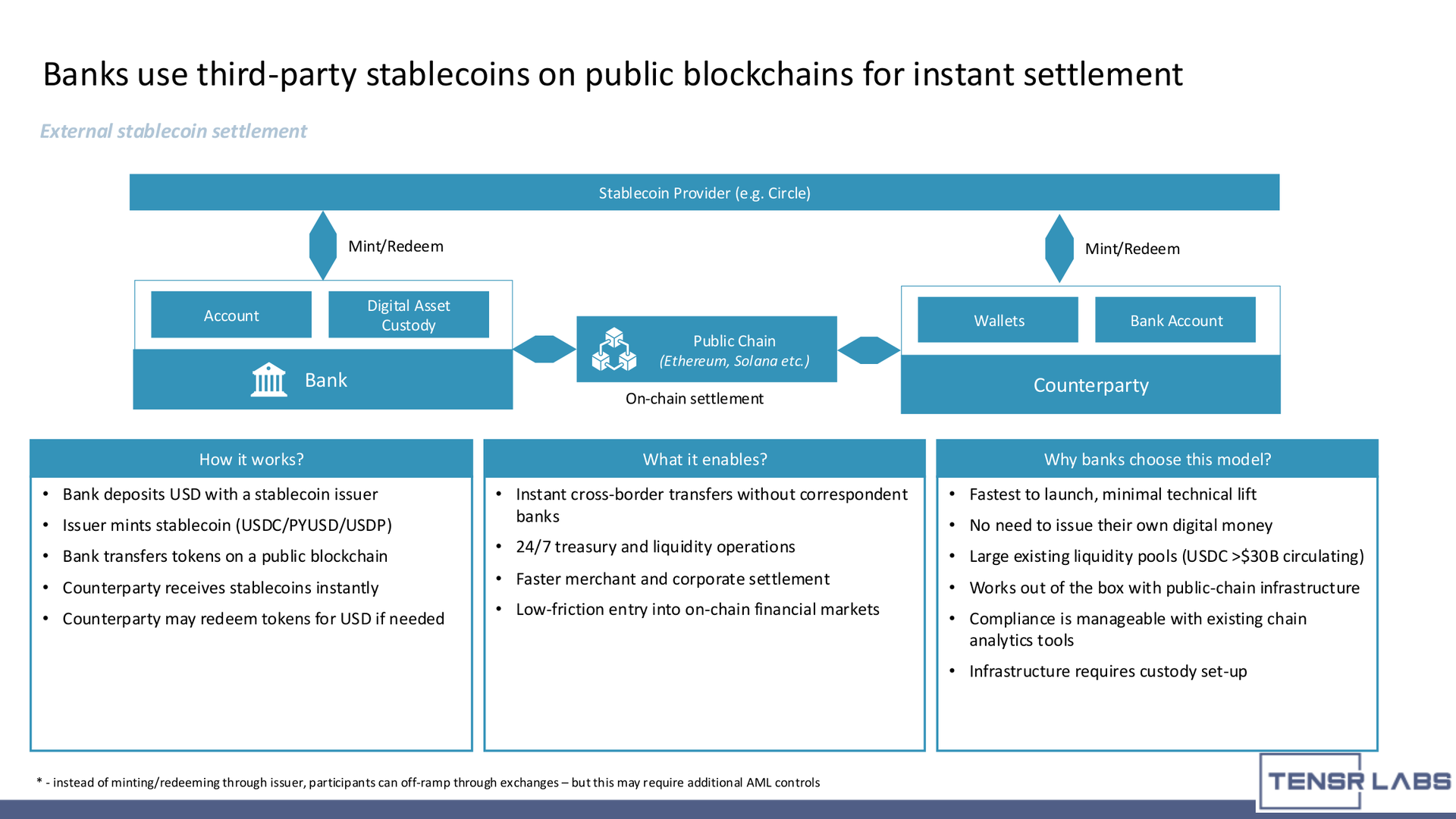

External Stablecoin Settlement: Fastest Path to Market

External stablecoin settlement uses regulated third-party stablecoins such as USDC, PYUSD, or USDP on public blockchains. The bank or fintech deposits fiat with an issuer, receives stablecoins, transfers tokens on-chain, and allows counterparties to hold or redeem them depending on the workflow.

This model is attractive because it is the fastest route to production. The institution does not need to issue its own digital cash or operate a private DLT network. It can use existing public-chain infrastructure, custody platforms, stablecoin issuers, and blockchain analytics tools.

External stablecoin settlement is well suited for:

- Neobanks and fintechs seeking quick time-to-market.

- PSPs and B2B payment providers moving value on-chain.

- Banks with active remittance or FX corridors.

- Treasury teams experimenting with 24/7 liquidity movement.

- Institutions that want public-chain access without building their own DLT.

Market signals are already substantial. JPMorgan has said JPM Coin handles more than $1 billion in daily transactions, as reported by Bloomberg and summarized by CoinDesk. PayPal USD is issued by Paxos Trust Company and is designed to be backed by U.S. dollar deposits, U.S. Treasuries, and cash equivalents, with public supply tracked across major market data venues and issuer resources such as Paxos. Circle's USDC reporting shows stablecoins moving into high-volume institutional and payment use cases, including the official State of the USDC Economy.

The implementation challenge is not only sending tokens. Banks still need custody setup, wallet policies, mint/redeem workflows, treasury reconciliation, counterparty screening, Travel Rule handling where applicable, and monitoring.

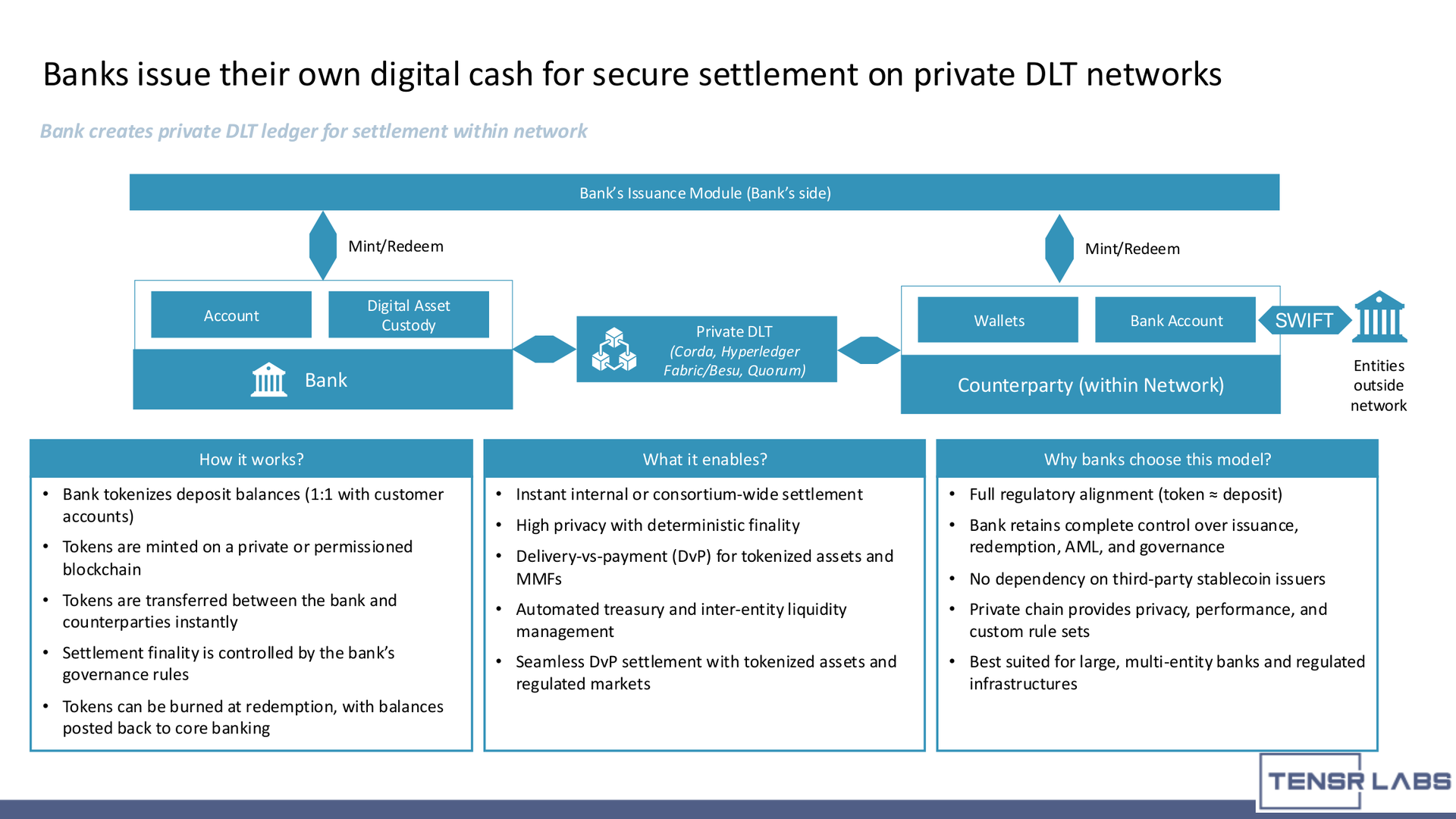

Tokenized Deposits: Bank-Issued Digital Cash for Controlled Settlement

Tokenized deposits are bank-issued digital representations of deposit balances, typically backed 1:1 by fiat deposits on the bank's ledger. Instead of using a third-party stablecoin issuer, the bank mints and burns digital cash against its own deposit records.

This model gives banks more control:

- The instrument remains closer to commercial bank money.

- Issuance and redemption are controlled by the bank.

- KYC, AML, governance, and wallet permissions can be embedded into the operating model.

- Settlement can occur on a private or permissioned DLT with deterministic finality.

- Privacy can be stronger than public-chain stablecoin settlement.

Tokenized deposits are well suited for:

- Large banks and global institutions.

- Banks with complex internal entity structures.

- Institutions implementing tokenized securities, MMFs, or DvP workflows.

- Banks seeking full control over settlement risk and governance.

- Inter-entity treasury and liquidity management.

In a typical architecture, the bank holds fiat deposits in its core ledger, mints matching tokens on a private DLT, allows approved participants to transfer those tokens instantly, and burns tokens at redemption while adjusting the fiat ledger. The token becomes a controlled settlement instrument tied to bank liabilities and internal governance.

This model is especially powerful for delivery-versus-payment. Tokenized deposits can act as the cash leg for tokenized securities, funds, or other digital assets, reducing settlement mismatch between asset and payment movement.

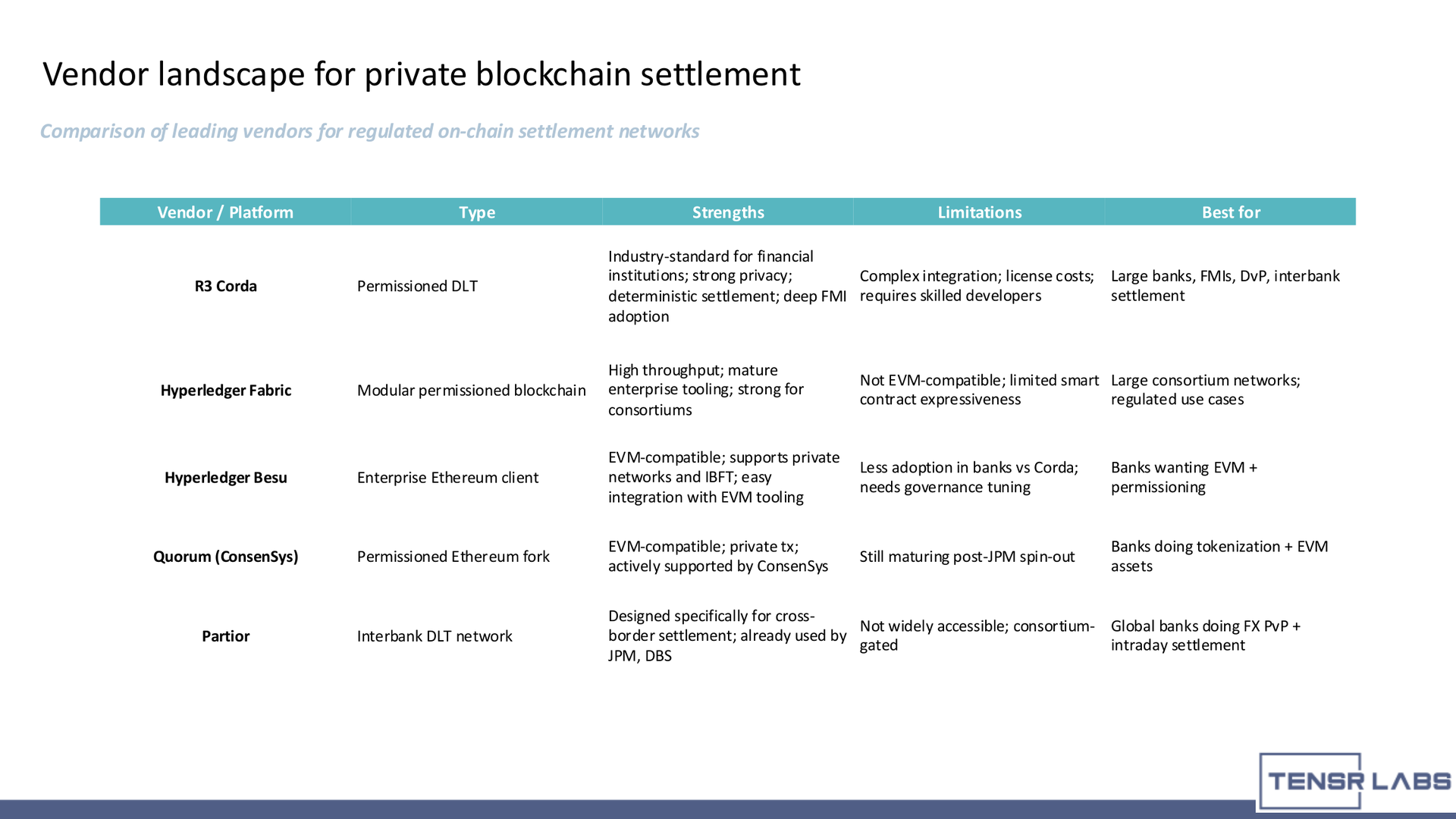

Private and Hybrid Settlement Networks

Private and hybrid settlement networks use permissioned DLT platforms such as Corda, Hyperledger Fabric, Hyperledger Besu, Quorum, Canton, or specialized interbank networks. They are designed for institutions that require privacy, deterministic finality, custom governance, and deeper control over participants.

These networks can support:

- Interbank settlement.

- Intragroup settlement across bank entities.

- Tokenized deposit movement.

- DvP with tokenized assets.

- FX payment-versus-payment and intraday liquidity workflows.

- Private market infrastructure and consortium models.

Private DLT is attractive when the bank or consortium needs control over identity, node roles, upgrade governance, data visibility, privacy, and dispute processes. It is also relevant where public-chain transparency or external issuer dependency is not acceptable.

Hybrid settlement is the long-term strategic direction for many institutions. A bank may use public stablecoins for certain corridors, tokenized deposits for controlled internal flows, and private DLT for high-value settlement. The digital settlement layer becomes the orchestration layer across those rails.

The challenge is complexity. Hybrid settlement requires interoperability, consistent governance, custody integration, liquidity management, compliance controls, and clear operating procedures across multiple rails.

Controls Banks Need Before Production

A digital settlement layer should be designed around controls first. The technology may move fast, but bank settlement cannot depend on unmanaged wallets or manual workarounds.

Before production, banks need:

- Custody and wallet governance: MPC or HSM-backed custody, wallet segregation, approval workflows, and operational wallet limits.

- Mint/redeem controls: clear procedures for stablecoin issuer flows or bank-issued tokenized deposit creation and burning.

- Network connectivity: reliable integration with public chains, private DLT platforms, RPC providers, nodes, or issuer APIs.

- Compliance screening: wallet screening, AML monitoring, sanctions checks, Travel Rule support where required, and counterparty risk scoring.

- Core-system reconciliation: ledger, treasury, payments, ERP, and finance integration so settlement activity is reflected in bank records.

- Policy engine: rules for asset, destination, amount, corridor, entity, user role, and approval path.

- Audit trail: evidence linking identity, approval, custody signing, blockchain transaction, settlement status, and reconciliation.

- Exception handling: runbooks for failed transfers, delayed confirmations, stuck transactions, off-ramp issues, and compliance escalations.

- Liquidity controls: thresholds, sweeps, reserve management, and visibility across hot, warm, cold, and settlement wallets.

- Governance: clear ownership across treasury, payments, compliance, operations, technology, and risk.

These controls are where most real implementation work happens. The blockchain rail provides movement. The settlement layer provides institutional safety.

How OQTACORE Can Help Implement Settlement Infrastructure

OQTACORE can help banks, fintechs, and institutional teams build digital settlement infrastructure across three stages.

For short-term rollout, OQTACORE can help implement public stablecoin settlement. That includes custody platform integration, wallet policies, mint/redeem workflows, treasury movement, compliance hooks, monitoring, and reconciliation.

For medium-term bank infrastructure, OQTACORE can help design private settlement layers for tokenized deposits, DvP, and intragroup settlement. This includes private DLT platform selection, governance model design, custody integration, workflow automation, and core-banking adapters.

For long-term multi-rail strategy, OQTACORE can help orchestrate settlement across stablecoins, tokenized deposits, private DLT networks, and interbank rails. The goal is to let institutions operate across multiple settlement models without creating separate control stacks for every product.

If your team is evaluating stablecoin settlement, tokenized deposits, or private DLT settlement, the first step should be an architecture review. The right question is not only which rail to choose. It is how custody, compliance, governance, liquidity, reconciliation, and auditability work together from day one.

CTA: Book a digital settlement architecture review with OQTACORE.

References

- BIS CPMI, SWIFT gpi data indicate drivers of fast cross-border payments

- SWIFT Payments Market Practice Group, Exceptions and investigations guidelines

- CoinDesk, JPMorgan handles $1B transactions daily in digital token JPM Coin

- Circle, State of the USDC Economy

- Paxos, PayPal USD

FAQs

A digital settlement layer is a bank-controlled infrastructure layer that connects core systems to public stablecoins, tokenized deposits, or private DLT networks. It manages wallet control, governance, compliance, network connectivity, monitoring, and reconciliation.

Banks or fintechs can use regulated stablecoins by depositing fiat with an issuer, receiving stablecoins, transferring tokens on a public blockchain, and reconciling the movement with treasury and payment systems. The model requires custody, wallet screening, mint/redeem controls, and monitoring.

Stablecoins are usually issued by third-party issuers and backed by reserves. Tokenized deposits are digital representations of bank deposit balances issued by the bank itself. Stablecoins can be faster to deploy, while tokenized deposits give banks more control over issuance, redemption, privacy, and governance.

A bank should consider private DLT when it needs stronger privacy, deterministic finality, participant governance, custom rules, interbank workflows, tokenized deposits, or DvP settlement with regulated digital assets.

Banks need custody, wallet governance, approval workflows, AML screening, policy engines, core-system reconciliation, liquidity controls, audit trails, exception procedures, and clear ownership across treasury, payments, compliance, operations, risk, and technology.